The recent push towards using market transactions to verify consensus data has been broadly embraced by the investment banking industry. The practice of using consensus data to value OTC derivatives originated in equities in the late 1990’s. It rapidly became a useful tool as an alternative to market quotes, transactions (including reference trades) and settlement values. All of these had flaws that created noise and uncertainty in the valuation process. Due to its reliability and stability, consensus was quickly established as the primary source of data for independent price verification (IPV) for OTC derivatives and it has subsequently been extended across all major asset classes to provide a robust and stable dataset for financial reporting.

Following the 2008 credit crisis, regulators have become increasingly concerned that consensus data is at risk of being blindly adopted and accepted without consideration of other market information. New initiatives have been launched to ensure that users of consensus data have the means to substantiate consensus using transaction data. “Back testing” is required. This is a natural and sensible progression as consensus valuations have become ingrained in the banking system.

Context has also changed. There has been a significant tightening of trading rules and a higher level of market surveillance since 2008, though the move to consensus substantiation should also come with some caveats and warnings.

Consensus data exists precisely because of the propensity for trades and quotes to be skewed, even in orderly markets. Traders can aggressively hit the bid and misquoted offers can be lifted in an instant. The definition used by most consensus providers to define the submitted price is “the price at which you are willing to trade with a similar sized market participant in a standard sized trade in an orderly market without undue stress”. Simply put – your trader’s best estimate of mid-market.

This is an important definition as highly volatile markets can bring out certain behaviours that influence trading decisions that would not be seen as desirable in an orderly market.

“Fear”, ”Greed” and ”Ego” drive much of the market fluctuations.

I cannot claim to have made these initial observations. That distinction goes back a long way to the inspirational leaders found on the trading floors of LIFFE and the CBOE who informed so much of my early learning.

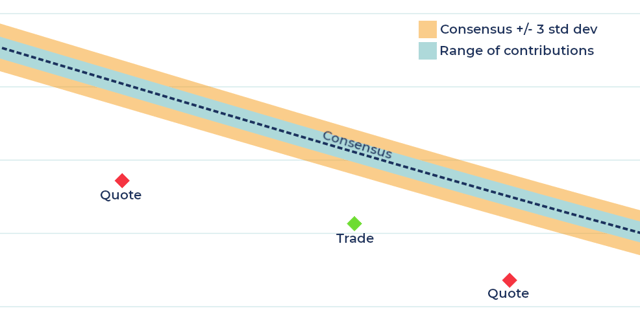

Let’s take an example from the European equity option markets on 17 March 2023, at the height of the storm surrounding the collapse of SVB.

Our graphic shows a snap taken from the implied volatility skew for the Dec-24 expiry on the Euro Stoxx 50 index. We show the consensus, the range of contributions, the +/- 3 standard deviations range, two “mid-market” OTC quotes” and a traded level, as labelled. It is clear that the consensus is away from observable market levels. Any attempt to back test consensus to the quotes and the traded level will conclude that consensus does not match transactions. Looking at the range of data forming the consensus, adjusting by 1, or even 2 standard deviations, will still result in a failure to match the traded levels. At 3 standard deviations most statisticians will be calling for the data to be classified as an outlier. And yet, it would be prudent to take the consensus over those trades every day of the week. And here is why.

All three transactions occurred between 6 and 8 hours before the market close. The previous day, there had been a rally in the market with volatility softening following the “shoring up” of Credit Suisse by the Swiss central bank. European markets opened strongly, only to fall sharply as banking shares continued to slump. Volatility rose suddenly as fear gripped the market once more. There were no reported OTC trades at that expiry date in outright options at the close of business.

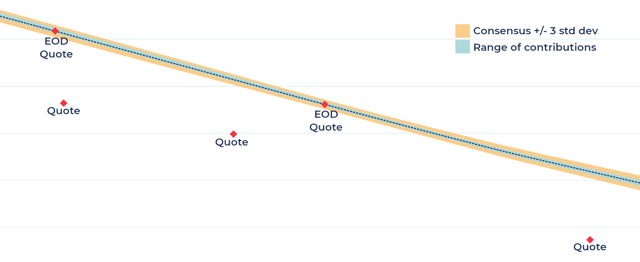

Our second chart shows a different expiry date on the same day. Once again we can see a number of mid-market quotes that are away from the consensus. Two quotes, printed within an hour of the close, lie on the consensus line.

Blindly including all quotes from earlier in the day in your IPV process without context will lead to skewed results. By comparison, there are hundreds of data points in the consensus grid that can be relied on every time in this situation. As fear grips the market, trades and quotes get blown away by rapid changes in implied volatility. Even in stable markets, ego can be a powerful motivator for trading behaviour, with “I am the market!” the rallying cry of aggressive, caffeine fueled traders. And Gordon Gecko has explained greed much better than I ever can or will.

Bringing together trades and consensus is a positive move and Skylight IPV continue to work with multiple vendors to bring the best value transaction data sources to our clients. It is an important innovation in the continuing evolution of consensus pricing, with exciting possibilities being explored by forward thinking firms in the industry. BUT here comes the caveat. Bringing trades and consensus together without understanding the factors that drive the market, is at best confusing and at worst may lead to a repeat of the errors that blighted the markets in the late 90s and early 00s.

Repeated analysis has proven that the consensus really is the most reliable source of information when markets are volatile. Transparent data sources with powerful analytics combined with expert knowledge and the right market participants are what makes consensus such a powerful resource for risk-conscious trading institutions.

At Skylight IPV we advocate a comprehensive, holistic approach to combining appropriate data sources for the purposes of IPV and related disciplines. Market information needs to be fed into an expert led framework that understands the provenance and nuances of the data for it to be applied correctly for the underlying valuation purpose.

Data sources must be transparent and explicable so that context can be applied with decisions audited and feedback assured. To completely rely on one type of data at the expense of all others, whether transaction or consensus data, would be to ignore the bigger picture. By combining transparency, expert opinion and high quality data sets from our industry leading partners we allow the facts to tell the story and empower industry stakeholders to embrace the wider context.

Adam McIlroy, CEO

Adam McIlroy, CEO