Basel II Prudent Valuation Guidance (page 161) defines Independent Price Verification (IPV) as:

“the process by which market prices or model inputs are regularly verified for accuracy. While daily marking-to-market may be performed by dealers, verification of market prices or model inputs should be performed by a unit independent of the dealing room, at least monthly (or, depending on the nature of the market/ trading activity, more frequently)”.

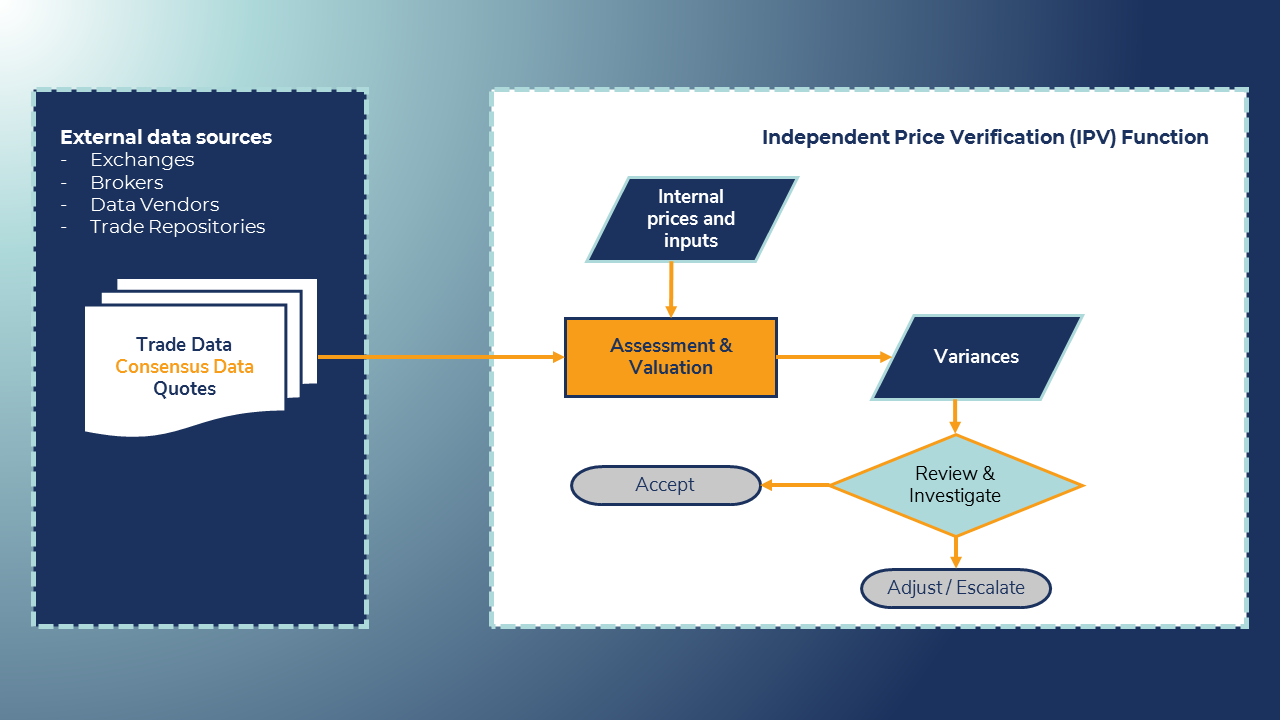

The IPV process thus requires that financial institutions’ internal prices or market data inputs, which generate the P&L of that institution, are verified against independently sourced data with a separation between the risk taking and control units.

IPV has grown to be one of the primary balance sheet controls and, over the 20 years that I was involved, has become increasingly important from a regulatory perspective. Incidents of trader mis-marking that have occurred over the years have pushed regulators to seek increased transparency and robustness in institutions’ IPV processes. These institutions have therefore invested substantial time and resources into developing both their systems and personnel to improve their IPV framework.

The core of the process is for the unit performing IPV to source the required data and to have the ability to revalue the books and records using contemporaneous independent data. That may be comparing mark-to-market prices directly or calculating the impact through the market data inputs where mark-to-model is implemented. Variances are generated against the trader marks and reported at the required levels (portfolio, desk, parameter, asset class, etc.). Where significant discrepancies between internal and independent prices occur, procedures should be in place to trigger an investigation, escalation and possible adjustments.

While conceptually IPV is relatively straightforward it can and does present multiple challenges, particularly in the cases where uncertainty driven by market illiquidity occurs or where highly bespoke trade structures may exist. In such cases those reviewing and analysing the variances need to possess the experience and technical knowledge to fully assess these situations, or have an escalation path to an individual or group that has the required skills. All staff involved with IPV should have the confidence to discuss results with traders, to challenge them where required and to escalate where necessary.

The independent data used in this verification process may come from multiple sources. These can include market exchanges, market transaction repositories, market brokers or consensus service vendors. With the volume of data required being extensive, consensus service vendors have the advantage of providing full data sets in a consistent format that can readily be processed by automated systems. This provides potential opportunities for a faster turnaround in the resolution of variance calculations and a greater frequency of IPV.

A good consensus vendor will have relevant expertise and will ensure that there is full transparency in their process. A “black box” approach should be avoided, and the full set of contributors’ submitted data should be accessible for investigative and analysis purposes.

Furthermore, where possible, transaction data sourced directly by the consensus vendor should be overlaid on the consensus data to flag potential issues as soon as possible. However, this should not abdicate the financial institution from performing additional checks and balances on the consensus data using transaction or broker data that may only be available to them.

This is only intended as a very high-level note on Independent Price Verification and its requirements and briefly touches on some of the pitfalls and nuances that can be encountered. Over time we hope to expand on some of these themes along with some related topics such as Fair Value Hierarchy and Prudential Valuation.

About the author

Andy received a PhD in Numerical Analysis and Programming from Dundee University before undertaking a series of academic positions across the globe. He moved into Finance with Banca Intesa Sanpaolo in Risk Management before taking senior roles in Product Control and Valuations with Deutsche Bank in 2004 and then Bank of America. He has been a leading voice in the development of IPV methodologies in that time.